# Shift-Share Instrumental Variables

```{r}

#| include: false

library(tidyverse)

library(fixest)

library(ggplot2)

library(knitr)

```

Shift-share, or Bartik, instruments combine local industry shares with

industry-level shocks. The idea is simple: a location with a large baseline

share in an industry is more exposed to shocks in that industry. The

difficult part is not constructing the instrument. The difficult part is

stating what is assumed exogenous: the shares, the shocks, or both.

## The construction

For each location $\ell$ and industry $k$, let $s_{\ell k}$ be the share of

local employment in industry $k$ at baseline, and let $g_k$ be a national

growth rate (or trade shock) for that industry. The shift-share instrument is

$$

B_\ell \;=\; \sum_{k=1}^{K} s_{\ell k}\, g_k.

$$

This is "shift-share" because it combines a local share with an

industry-level shift. @bartik-1991 used local industry mix to predict local

employment growth. @autor-dorn-hanson-2013 used local industry shares

interacted with industry-level Chinese import growth in other high-income

countries.

The first-stage regression is then

$$

\Delta L_\ell \;=\; \pi_0 + \pi_1 B_\ell + X_\ell'\gamma + \epsilon_\ell,

$$

with $B_\ell$ instrumenting for the observed local shock in a 2SLS for the

outcome of interest.

## Two identification views

There are two ways to justify a shift-share instrument. They put the

exogeneity assumption on different objects.

### Share view (GPSS 2020)

Treat the shares $s_{\ell k}$ as the source of identifying variation, with the

shocks $g_k$ acting as weights. The instrument is valid if shares are

exogenous to the outcome (conditional on controls).

@goldsmith-pinkham-sorkin-swift-2020 (henceforth GPSS) prove that the

shift-share IV is numerically equivalent to a GMM combination of $K$

just-identified IVs, one per industry share:

$$

\hat\beta^{SS} \;=\; \sum_{k=1}^{K} \hat\alpha_k\, \hat\beta_k,

$$

where $\hat\beta_k$ is the just-identified IV using share $s_{\cdot k}$ alone

and $\hat\alpha_k$ is the **Rotemberg weight**. This gives an important

diagnostic: which industry shares are driving the estimate?

### Shock view (BHJ 2022)

Treat the shocks $g_k$ as the source of identifying variation. Shares are

exposure weights. Under this view, shocks should be uncorrelated with the

second-stage unobservables, conditional on industry-level controls.

@borusyak-hull-jaravel-2022 (henceforth BHJ) show how to rewrite the

regression at the shock level.

The two views are not mutually exclusive. In an application, we should be

clear which one is being defended and report diagnostics for both.

## Inference

Standard OLS or cluster-robust standard errors on the regional regression

**underestimate uncertainty** because the same industry shocks appear in many

regions, inducing cross-region correlation that region-level clustering does

not capture. Two corrections are now standard:

- **Cluster on shocks (BHJ)**: equivalent to running the regression at the

industry-shock level. Implemented via shock-level reweighting.

- **AKM SE** [@adao-kolesar-morales-2019]: explicit formula for SE accounting

for shock-level correlation. Available in the `ShiftShareSE` R package.

## Simulation: build intuition

Use a small DGP with regions, industries, and a known causal effect.

```{r}

#| label: sim-data

#| cache: true

n_region <- 500

n_industry <- 20

beta_true <- 0.5

df <- read_csv("data/shift_share_sim.csv", show_col_types = FALSE)

shares <- as.matrix(read_csv("data/shift_share_shares.csv", show_col_types = FALSE))

# This simulation is constructed to satisfy the Borusyak et al. (2022)

# shock-exogeneity assumption: the industry-level shocks are drawn

# independently of the region-level confounder `u` and of the shares

# themselves. The shares are allowed to be endogenous (correlated with

# region characteristics) -- it is specifically the shocks that must be

# "as good as randomly assigned" for this identification argument, which is

# a different (and in this simulation, the maintained) assumption from the

# Goldsmith-Pinkham et al. (2020) shares-exogeneity view discussed above.

shocks <- read_csv("data/shift_share_shocks.csv", show_col_types = FALSE)$shock

u <- df$u

head(df)

```

A naive OLS suffers from the confounder `u`:

```{r}

#| label: naive-ols

#| cache: true

ols <- feols(Y ~ X, data = df)

ivss <- feols(Y ~ 1 | X ~ B, data = df)

etable(ols, ivss, headers = c("OLS", "Shift-share IV"),

digits = 3, digits.stats = 3, fitstat = ~ . + ivf)

```

OLS is biased upward by the confounder; the shift-share IV recovers a

value close to the true effect of `r beta_true`. With concentrated industry

shares and 20 industries, the first-stage F is well above 100.

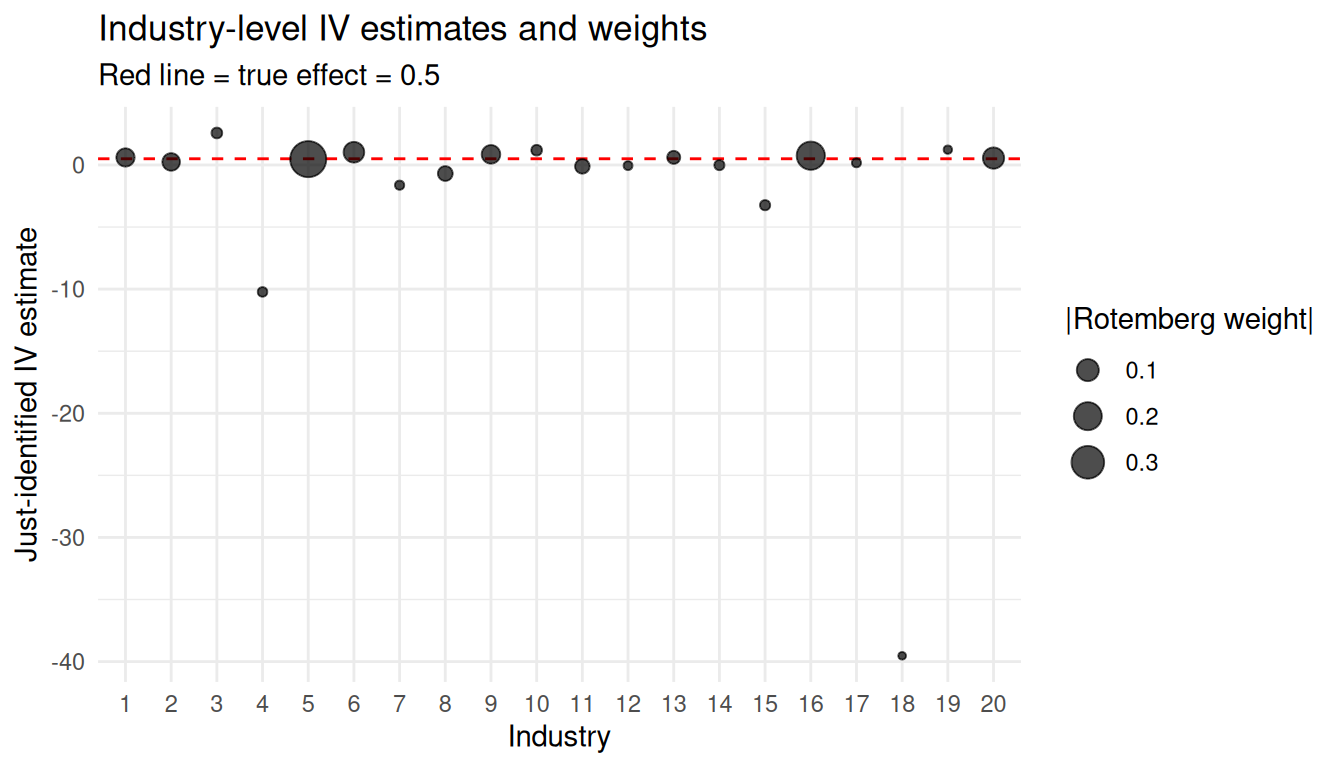

### Rotemberg weights

The GPSS decomposition says the shift-share IV is a weighted average of

$K$ just-identified IVs (one per industry share). Compute the weights:

```{r}

#| label: rotemberg

#| cache: true

# Rotemberg weight for industry k (using centered moments to match the

# demeaned 2SLS regression):

# alpha_k = g_k * Cov(s_{.k}, X) / sum_j g_j * Cov(s_{.j}, X)

# Each industry's just-identified IV estimate uses s_{.k} as instrument:

# beta_k = Cov(s_{.k}, Y) / Cov(s_{.k}, X)

# GPSS prove the shift-share IV estimate equals sum_k alpha_k * beta_k.

cov_sk_X <- sapply(1:n_industry, function(k) cov(shares[, k], df$X))

cov_sk_Y <- sapply(1:n_industry, function(k) cov(shares[, k], df$Y))

denom <- sum(shocks * cov_sk_X)

alpha <- shocks * cov_sk_X / denom

beta_k <- cov_sk_Y / cov_sk_X

rotemberg <- tibble(industry = 1:n_industry,

shock = shocks,

weight = alpha,

beta_k = beta_k)

kable(rotemberg, digits = 3,

caption = paste0("Rotemberg decomposition. Sum of alpha*beta_k = ",

round(sum(alpha * beta_k), 3),

" (= shift-share IV estimate of ",

round(coef(ivss)["fit_X"], 3), ")."))

```

Two diagnostics matter:

1. **Weight concentration**: if one or two industries carry most of the

weight, the identifying variation is essentially coming from those

industries' shares. Their exogeneity is the assumption you're really

leaning on.

2. **Heterogeneous $\hat\beta_k$**: in this benign simulation, the

industry-specific IVs are all near the true effect (with sampling noise).

In real data, if a few industries give wildly different estimates, the

"average" shift-share IV is averaging over heterogeneous treatment effects

you should report explicitly.

```{r}

#| label: rotemberg-plot

#| cache: true

#| fig-height: 4

#| fig-width: 7

ggplot(rotemberg, aes(x = factor(industry), y = beta_k, size = abs(weight))) +

geom_hline(yintercept = beta_true, linetype = "dashed", color = "red") +

geom_point(alpha = 0.7) +

scale_size_continuous(name = "|Rotemberg weight|") +

labs(x = "Industry", y = "Just-identified IV estimate",

title = "Industry-level IV estimates and weights",

subtitle = paste("Red line = true effect =", beta_true)) +

theme_minimal()

```

### What goes wrong when shares are endogenous

Now break the share-exogeneity assumption: make industry 1's share correlated

with the second-stage error.

```{r}

#| label: bad-shares

#| cache: true

# Re-do shares so industry 1's share covaries with a new confounder v

v <- read_csv("data/shift_share_bad_v.csv", show_col_types = FALSE)$v

shares_bad <- shares

shares_bad[, 1] <- pmax(0.01, shares[, 1] + 0.15 * v)

shares_bad <- shares_bad / rowSums(shares_bad) # renormalise to sum to 1

bad_noise <- read_csv("data/shift_share_bad_noise.csv", show_col_types = FALSE)

B_bad <- as.numeric(shares_bad %*% shocks)

X_bad <- B_bad + 0.3 * u + bad_noise$noise_x

Y_bad <- beta_true * X_bad + u + 0.6 * v + bad_noise$noise_y

df_bad <- tibble(X = X_bad, Y = Y_bad, B = B_bad)

ivss_bad <- feols(Y ~ 1 | X ~ B, data = df_bad)

cat("True beta:", beta_true, "\n")

cat("Shift-share IV with bad share 1:", round(coef(ivss_bad)["fit_X"], 3), "\n")

# Rotemberg weights recomputed under the bad shares

cov_sk_X_bad <- sapply(1:n_industry, function(k) cov(shares_bad[, k], X_bad))

alpha_bad <- shocks * cov_sk_X_bad / sum(shocks * cov_sk_X_bad)

cat("Rotemberg weight of industry 1:", round(alpha_bad[1], 3),

"-- rank", rank(-abs(alpha_bad))[1], "of", n_industry, "\n")

# Leave-one-industry-out: rebuild the instrument without industry 1

B_loo <- as.numeric(shares_bad[, -1] %*% shocks[-1])

ivss_loo <- feols(Y ~ 1 | X ~ B, data = tibble(X = X_bad, Y = Y_bad, B = B_loo))

cat("Shift-share IV without industry 1:", round(coef(ivss_loo)["fit_X"], 3), "\n")

```

The estimate is biased, and the bias comes from one industry's share being

related to the error. Note which diagnostic catches it. Rotemberg weights

measure *influence* --- whose exogeneity the estimate leans on --- not

endogeneity: the offending industry carries a weight of only 0.11, third

largest of twenty, yet it alone moves the estimate from 0.5 to 0.8. The

leave-one-industry-out check is what isolates it: rebuilding the instrument

without industry 1 restores the estimate to 0.48.

## Empirical: the China shock (Autor, Dorn, Hanson 2013)

The standard shift-share application is the China-shock study of

@autor-dorn-hanson-2013 (henceforth ADH). Commuting zones are exposed

differently to Chinese import competition because their baseline industry

mixes differ. The instrument is

$$

\text{IV}_\ell \;=\; \sum_k \frac{L_{\ell k,\,1990}}{L_{\ell,\,1990}}\,

\frac{\Delta M^{other}_{k}}{L_{k,\,1990}},

$$

where the shocks $\Delta M^{other}_k$ are growth in Chinese imports into

other high-income countries. This leave-one-out construction removes

US-specific demand from the shock. In the actual ADH design the employment

shares are lagged one census behind the outcome period (e.g. 1980 employment

for the 1990--2000 stack), precisely to mitigate share endogeneity; we date

everything to 1990 here to keep the notation light.

```{r}

#| label: adh-skeleton

#| eval: false

#| echo: true

# David Dorn distributes the replication data at

# https://www.ddorn.net/data.htm — files needed:

# workfile_china.dta (commuting zone data, 1990-2007)

# industry_shares.csv (czone-industry shares)

# industry_imports.csv (industry-level imports)

library(haven)

library(fixest)

cz <- read_dta("workfile_china.dta")

fit <- feols(d_sh_empl_mfg ~ 1 | d_tradeusch_pw ~ d_tradeotch_pw_lag,

data = cz,

cluster = ~ statefip)

summary(fit)

```

Modern best-practice extensions of the basic ADH regression. These blocks are

schematic --- they do not run here, so check argument names against the

current package documentation before adapting them:

```{r}

#| label: adh-modern

#| eval: false

#| echo: true

# 1. Rotemberg weights via the bartik.weight package (Goldsmith-Pinkham)

# devtools::install_github("paulgp/bartik-weight")

library(bartik.weight)

rw <- bw(cz, master = master_spec, y = "d_sh_empl_mfg",

x = "d_tradeusch_pw", weight = "timepwt48",

G = G_growth, Z = Z_shares)

# Plot the Rotemberg weights to see which industries drive the estimate

plot(rw)

# 2. Adão-Kolesár-Morales standard errors

# devtools::install_github("kolesarm/ShiftShareSE")

library(ShiftShareSE)

ivreg_ss(d_sh_empl_mfg ~ d_tradeusch_pw + controls,

X = "d_tradeotch_pw_lag",

data = cz, W = shock_weights, region_cvar = "czone",

method = "akm0")

# 3. BHJ shock-level inference: collapse to shock (industry-period) level

# devtools::install_github("borusyak/shift-share")

library(ssaggregate)

shocks_data <- ssaggregate(data = cz, vars = c("d_sh_empl_mfg",

"d_tradeusch_pw"),

shock = "d_tradeotch_pw_lag", weights = "timepwt48",

l = "czone", n = "industry", t = "year",

s = "share")

# Now regress at shock level — interpretation: shock-level IV

feols(d_sh_empl_mfg ~ 1 | d_tradeusch_pw ~ shock, data = shocks_data)

```

For a new shift-share paper, I would expect Rotemberg weights, AKM standard

errors, and a BHJ shock-level version or an explanation for why it is not

appropriate.

## Summary

- Shift-share IV combines local shares and industry shocks.

- The GPSS view puts exogeneity on shares; the BHJ view puts it on shocks.

- Rotemberg weights show which industry shares drive the 2SLS estimate.

- Region-level clustering is usually too optimistic. Use AKM standard errors

or shock-level inference when possible.

- In R, `fixest`, `bartik.weight`, `ShiftShareSE`, and `ssaggregate` cover

most of the workflow.